Best Personal Loans 2026: Top 7 Picks for Every Credit Score in US

In 2026, the personal loan market has shifted toward “Hyper-Personalized Lending.” Traditional FICO scores are still relevant, but the best lenders now use real-time cash flow analysis to offer lower rates to borrowers who were previously overlooked. Whether you are consolidating high-interest debt or funding a major life event, choosing the right partner can save you thousands in interest.

Before applying, ensure you have checked your 2026 Credit Health Report to ensure you qualify for the lowest advertised rates.

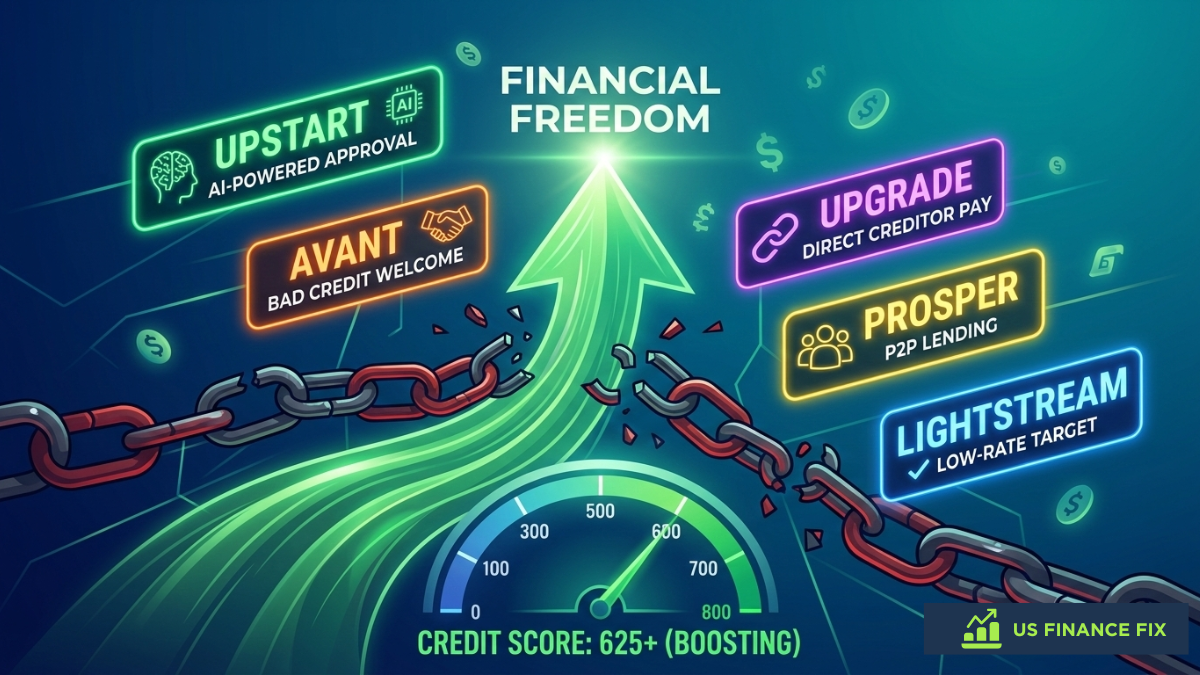

The Top 7 Personal Loan Lenders of 2026

We have vetted dozens of providers based on APR, transparency, and “speed to fund.” Here are our top picks for this year:

- SoFi: Best for High-Earners & Career Coaching. (Best for: Excellent Credit)

- LightStream: Best for Home Improvement & Low Rates. (Best for: Good to Excellent Credit)

- Upgrade: Best for Fast Funding & Credit Building Tools. (Best for: Fair Credit)

- Upstart: Best for Borrowers with Short Credit Histories. (Uses AI to look beyond FICO)

- Marcus by Goldman Sachs: Best for No-Fee Debt Consolidation.

- Best Egg: Best for Secured Loan Options to Lower APR.

- Avant: Best for Rebuilding Credit and Transparent Terms. (Best for: Poor to Fair Credit)

Best Personal Loans 2026 Comparison: At a Glance

| Lender | Est. APR Range | Max Amount | Min. FICO | Origination Fee | Time to Fund |

|---|---|---|---|---|---|

| SoFi | 8.74% – 35.49% | $100,000 | 680+ | 0% – 7% | Same-Day / 24hrs |

| LightStream | 6.49% – 25.29% | $100,000 | 660+ | None | Same-Day |

| Upstart | 6.20% – 35.99% | $50,000 | None | 0% – 12% | 1–3 Business Days |

| Upgrade | 7.74% – 35.99% | $50,000 | 600+ | 1.85% – 9.99% | 1 Business Day |

| Best Egg | 6.99% – 35.99% | $50,000 | 600+ | 0% – 8.99% | 1–3 Business Days |

| Discover | 7.99% – 24.99% | $40,000 | 660+ | None | Next Day |

| Avant | 9.95% – 35.99% | $35,000 | 550+ | Up to 4.75% | 1–2 Business Days |

*Lowest rates often require Autopay and excellent credit history. APRs updated as of March 2026.

A Closer Look: The 2026 Market Leaders

1. SoFi: The Best Overall for High-Earners

SoFi remains the “Gold Standard” in 2026 for borrowers with strong credit profiles. Their model has evolved beyond simple lending into a full “Career and Wealth” ecosystem.

- The 2026 Advantage: Beyond the loan, SoFi offers “Member Perks” like free career coaching, estate planning discounts, and a 0.25% APR reduction if you set up direct deposit into their high-yield checking account.

- Fast-Track Funding: In many cases, if you apply before 10:00 AM, funds can be in your account by the end of the business day.

- Unemployment Protection: One of their standout features is the ability to temporarily pause payments if you lose your job through no fault of your own, helping you avoid a credit disaster during a career transition.

2. LightStream: Best for Home Improvement & Low Rates

As a division of Truist, LightStream is the “no-nonsense” lender for those who have spent years building excellent credit.

- The “Rate Beat” Program: LightStream is famous for their 2026 commitment to beat any competitor’s rate by 0.10 percentage points if the terms are identical.

- No Fees, Period: They are one of the few remaining lenders that charge absolutely zero origination, late, or prepayment fees. What you see is exactly what you get.

- Large-Scale Projects: With loan limits up to $100,000 and terms extending out to 12 years for specific home projects, they are the top choice for 2026 homeowners looking to avoid high-interest HELOCs.

3. Upstart: Best for “Thin” Credit Files & AI Underwriting

Upstart has revolutionized the 2026 lending market by looking at more than just a FICO score. This is the go-to for young professionals or those who are new to the U.S. credit system.

- The “Holistic” Model: Their AI-driven platform considers your education, job history, and even your area of study to predict your creditworthiness.

- High Approval Rates: Because they use non-traditional data, Upstart often approves borrowers that traditional banks might reject, though this usually comes with a higher APR compared to SoFi or LightStream.

- Instant Verification: By linking your bank account through secure 2026 “Open Banking” protocols, Upstart can often verify your income and identity in seconds without requiring paper paystubs.

💡 Alex Hale Pro-Tip: The 2026 “Soft-Pull” Strategy

Before you commit to a single lender, use the Soft-Pull Method. In 2026, almost every major online lender allows you to see your personalized rate and term without a “Hard Inquiry” on your credit report. We recommend checking at least three of the lenders above to compare the Total Interest Cost before making your final selection.

How to Apply for a Personal Loan in 2026

Applying for a personal loan has evolved. While your FICO score still matters, 2026 lenders now prioritize real-time data and “Agentic AI” to verify your eligibility instantly. To ensure you get the lowest possible APR, follow our verified 5-step checklist below.

Step 1: Check Your 2026 Credit Health Report

Before you apply, pull your latest report. In 2026, lenders aren’t just looking at a three-digit number; they are looking for “Clean Liquidity”—proof that you haven’t taken on too many new buy-now-pay-later (BNPL) obligations in the last 60 days.

Step 2: Gather Your Digital Income Proof

Gone are the days of scanning paper paystubs. Most top-tier lenders now use Open Banking APIs (like Plaid or Mastercard Open Finance). You’ll likely simply link your primary checking account to the lender’s portal to verify your “Cash Flow Underwriting” in seconds.

Step 3: Reduce Your Revolving Debt (The 30% Rule)

To trigger the lowest “Excellent Credit” rates, try to bring your credit card utilization below 30% at least two weeks before applying. AI underwriting models in 2026 are highly sensitive to sudden drops in revolving balances.

Step 4: Calculate Your “Total Capital Need”

Don’t just guess. Borrowing $500 too much can sometimes push you into a higher “risk tier,” increasing your APR. Use a loan calculator to find the exact amount needed for your debt consolidation or home project to keep your Debt-to-Income (DTI) ratio lean.

Step 5: Perform a “Soft-Pull” Comparison

Never settle for the first offer. Use the Soft-Pull Method to compare at least three lenders from our Top 7 Picks list. This allows you to see your personalized 2026 interest rate and term without any impact on your credit score.

💡 Alex Hale Pro-Tip: The “Thin-File” Hack for 2026

No FICO? No Problem. If you have a limited credit history (a “thin file”), traditional lenders might reject you automatically. However, in 2026, several “AI-First” lenders like Upstart and LendingPoint have moved beyond the 3-digit score.

The Strategy: Use a lender that offers Cash Flow Underwriting. By securely linking your bank account via Open Banking (Plaid), these lenders analyze your real-time income stability and spending habits rather than just your past credit mistakes. If you can show 90 days of consistent deposits and a positive balance, you can often secure a “Good Credit” rate even with a “Fair” or non-existent score.

Strategic Borrowing in 2026

Interest rates in 2026 remain sensitive to Federal Reserve shifts. When comparing loans, look beyond the monthly payment and focus on the Total Cost of Capital. A loan with a lower monthly payment but a longer term can often cost double in total interest.

If your goal is debt consolidation, ensure the loan’s APR is at least 5% lower than your current credit card rates to make the math work in your favor. You can check current national averages via the Federal Reserve Consumer Credit Report.

Best Personal Loans 2026: FAQs

What is the average personal loan interest rate in 2026?

While rates vary by credit tier, the 2026 average for excellent credit (720+) hovers between 7% and 11%, while fair credit borrowers may see rates from 18% to 28%.

Do personal loans hurt my credit score?

Initially, you may see a small dip of 5–10 points due to a “Hard Inquiry.” However, if you use the loan to pay off revolving credit card debt, your score often bounces back higher within 60 days due to improved credit utilization.

Are there “No-Fee” loans available?

Yes. Many top-tier lenders like SoFi and Marcus have eliminated origination fees, late fees, and prepayment penalties. Always check the “Schumer Box” or disclosure statement before signing.

How fast can I get funds in 2026?

Thanks to instant bank verification, many online lenders can now deposit funds into your account within 24 to 48 hours of approval.

Should I choose a fixed or variable rate loan?

In the current 2026 economic climate, we generally recommend Fixed-Rate Loans. This protects you from future rate hikes and ensures your monthly payment remains predictable throughout the life of the loan.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.