Beginner Investing Guide 2026: From Debt-Free to Wealth-Builder

Congratulations. If you have followed our guides on student loan repayment and debt consolidation, you have earned the right to focus on the most exciting part of personal finance: Wealth Creation.

In 2026, you don’t need thousands of dollars to be an “investor.” Between fractional shares and zero-commission platforms, the barrier to entry has vanished. The goal now is consistency and understanding where your next dollar should live to grow the fastest.

The 2026 Priority List: Where to Put Your Money First

Before you chase the next viral stock, you must follow the 2026 “Order of Operations.” This ensures you are capturing guaranteed returns (like employer matches) before taking market risks.

- The Employer Match (The 100% Return): If your job offers a 401(k) or 403(b) match, this is your non-negotiable first stop. It is a guaranteed 100% return on your investment—a mathematical certainty you will never find in the open market.

In 2026, many employers have automated these contributions; ensure yours is set to at least the “maximum match” threshold to avoid leaving thousands in “free money” on the table over your career. - The Roth IRA Shield: In 2026, tax-advantaged growth is your greatest ally against inflation. Unlike a traditional 401(k), a Roth IRA is funded with “post-tax” dollars, meaning every penny of growth and every future withdrawal is 100% tax-free.

This “shield” is vital for beginners because it allows your money to compound without a future tax bill lurking at the finish line. If you are under the income limit, prioritize this immediately after securing your employer match. - Taxable Brokerage (The “Flex” Bucket): Once your retirement buckets are handled, use a standard brokerage account for “mid-term” goals – those 5 to 10 years away, like a home down payment or starting a business.

While you don’t get the same tax shields here, you gain total liquidity. In 2026, we utilize these accounts to house low-cost index funds and fractional shares, ensuring your “extra” cash is working harder than it would in a standard savings account.

The Power of Fractional Shares and Index Funds

The “New Rules” of 2026 allow you to own a piece of the world’s most expensive companies for as little as $1. Fractional shares mean you no longer have to wait until you can afford a full share of a $3,000 stock to start growing your portfolio.

However, for most beginners, Index Funds are the superior choice. Instead of betting on one company, you are betting on the entire economy. It’s the ultimate “set it and forget it” strategy that beats most professional stock pickers over the long term.

To see how your current savings might grow over time, you can use the SEC Compound Interest Calculator to visualize the “Snowball Effect.”

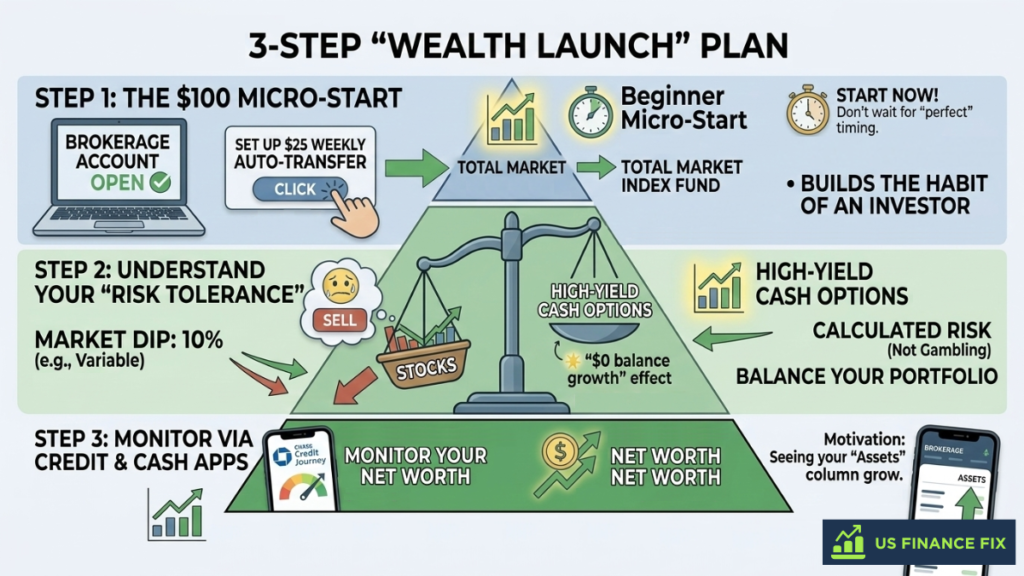

Alex’s 3-Step “Wealth Launch” Plan

- Step 1: The $100 Micro-Start (Breaking the Inertia): Don’t wait for “perfect” timing or a massive windfall to begin. Open a brokerage account today and set up a $25 weekly auto-transfer into a total market index fund. In 2026, fractional shares make it possible to own the world’s largest companies with just a few dollars. This isn’t just about the money; it’s about building the habit of an investor and proving to yourself that you can grow assets while managing daily expenses.

- Step 2: Understand Your “Risk Tolerance” (Calculated Growth): Investing isn’t gambling; it is the management of calculated risk. A simple litmus test for 2026: if a 10% market dip makes you want to panic-sell, your portfolio is too aggressive for your current stage. To stay the course, balance your stock market exposure with high-yield cash options or money market funds. This “ballast” keeps your portfolio stable, ensuring you don’t abandon your strategy during normal market cycles.

- Step 3: Monitor via Credit & Cash Apps (The Motivation Loop): Just as you used Chase Credit Journey to watch your score rise, use your brokerage app to monitor your Net Worth. Seeing your “Assets” column grow is the ultimate psychological fuel to keep going. By tracking your total value rather than just daily stock fluctuations, you shift your focus from “spending” to “accumulating,” which is the hallmark of a true wealth-builder.

Beginner Investing Guide 2026: FAQs

How much money do I need to start investing in 2026?

You can start with as little as $1. Most modern platforms allow for fractional share investing, meaning you can buy $5 worth of a major tech stock or index fund immediately.

What is the difference between a 401(k) and a Roth IRA?

A 401(k) is usually offered through an employer and often includes a “match.” A Roth IRA is an individual account you open yourself. The main difference is when you pay taxes: 401(k)s are typically “pre-tax,” while Roth IRAs are “post-tax,” allowing for tax-free withdrawals later.

Is the stock market safe for my emergency fund?

No. Never invest money you might need in the next 12 months. Your emergency fund should stay in a high-yield savings account. Investing is for “long-term” money (5+ years).

What is an Index Fund?

Think of an Index Fund as a basket of hundreds of different stocks. When you buy one share of the fund, you own a tiny piece of all those companies at once, which diversifies your risk automatically.

How do I pick the “best” stocks?

For beginners, the “best” stock is often no stock at all—it’s an Exchange Traded Fund (ETF) or Index Fund. Trying to pick individual winners is difficult; it’s much safer to follow the analytical approach we use for debt: look at the historical data and lower your costs.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.