Best High-Yield Savings Accounts in the US: 2026 Top Picks

Traditional big banks still pay a measly 0.01%. These 7 best high-yield savings accounts 2026 pay up to 5.25% APY – turning your stagnant cash into a growing emergency fund. No hidden fees, FDIC insured, and a 5-minute online setup. Updated for March 2026.

Quick math: $10K at 5% = $500/yr vs $1/yr at 0.01%.

Why High-Yield Savings Accounts is a Must-Have

If your money is sitting in a “big bank” savings account, you’re essentially giving the bank a free loan. Here is why you should make the switch today:

- Make Your Emergency Fund Work: Most experts suggest saving 3–6 months of expenses. In a high-yield account, that safety net actually grows. A $10,000 fund at 5% APY earns you about $40 every month – enough to cover a streaming subscription or a nice lunch.

- Reach Your Goals Faster: Saving for a car, a wedding, or a house? High-yield interest acts like a “bonus” that gets you to your goal months ahead of schedule.

- Maximum Safety, Zero Risk: Unlike the stock market, your money is 100% safe. It’s protected by the government (FDIC) up to $250,000, so you get high returns without the stress of losing a penny.

Our 2026 Selection Criteria: How We Rank These Accounts

At US Finance Fix, we don’t just chase the highest decimal point. A 5.50% rate is useless if the app crashes or the bank has hidden fees. We rank these accounts based on four non-negotiable pillars:

- FDIC/NCUA Insurance: Every account on this list is government-backed up to $250,000.

- Fee Transparency: We prioritize “No-Fee” banks. If there’s a monthly maintenance fee, it doesn’t make the list.

- Transfer Speed: An emergency fund is useless if you can’t access it. We test for 1–2 business day transfer speeds.

- User Experience: We favor banks with highly-rated mobile apps (4.5+ stars) so you can manage your cash on the go.

7 Best High‑Yield Savings Accounts 2026: Comparison

| Bank | APY | Min Deposit | Fees | ATM | Best For | Opening Link |

|---|---|---|---|---|---|---|

| Digital Federal Credit Union | 5.00% (on first $1,000) | $0 | $0 | 30K free | Small Emergency Funds | Open → |

| Varo Bank | 5.00% (up to $5,000)* | $0 | $0 | Unlimited | Mobile-First Savers | Open → |

| AdelFi | 5.00% (up to $5,000) | $25 | $0 | Limited | Christian Values-Based Banking | Open → |

| Bask Bank | 4.00% (with Rate Boost) | $0 | $0 | No | Simple Interest | Open → |

| EverBank | 3.90% (New Accounts) | $0 | $0 | Yes | Large Balances | Open → |

| Citizens Access | 3.15% | $0 | $0 | No | Citizens customers | Open → |

| SoFi Checking & Savings | 3.30% – 4.00%* | $0 | $0 | 55K free | All‑in‑One banking | Open → |

*Varo and SoFi rates typically require a qualifying direct deposit to unlock the highest tier.

Rates verified March 5, 2026. Rates are variable and subject to change.

HYSA vs. CD: Where Should Your Cash Live in 2026?

With the Federal Funds rate at 4.25-4.50%, many readers ask: “Should I lock in a Certificate of Deposit (CD) rate or stay in a High-Yield Savings Account?”

- Choose an HYSA if: You are building an Emergency Fund. You need liquidity. If your car breaks down tomorrow, you can’t wait for a 12-month CD to mature.

- Choose a CD if: you have “extra” cash (like a house down payment) that you won’t need for at least a year.

Alex’s Tip: In a “high-rate environment” like we have now, I recommend a Hybrid Strategy. Keep 3 months of expenses in a liquid HYSA (like Digital Federal Credit Union) and move the rest into a 12-month CD to “lock in” these 5% yields before the Fed potentially cuts rates later this year.

Digital Federal Credit Union (DCU): The 2026 High-Rate Leader

DCU is a member-owned credit union that consistently outpaces national banks by returning profits to its members in the form of higher yields. In 2026, it remains the “gold standard” for savers who want a top-tier rate without the volatility of smaller fintech startups.

- The Standout Feature: Their Primary Savings Account offers an industry-leading 5.25% APY on your first $1,000, making it the perfect “seed” account for a new emergency fund.

- Why it Wins: Unlike big banks that require massive balances for high rates, DCU offers this elite yield with a $0 minimum balance and provides access to over 30,000 surcharge-free ATMs nationwide.

Bask Bank: The Pure Play for High Interest

Bask Bank is a digital-only division of Texas Capital Bank. They are perfect for the “minimalist” saver who wants the absolute highest yield without needing a checking account or extra bells and whistles.

- The Standout Feature: No tiers or “hoops.” You get the top rate on every dollar from $0.01 to $2 million.

SoFi: The Best All-In-One Banking Suite

If you want to replace your “Big Bank” (Chase/Wells Fargo) entirely, SoFi is the 2026 winner.

- The Standout Feature: You get the high 4.30%+ APY on both Savings and Checking, as long as you have a direct deposit. Plus, you get up to $2M in FDIC insurance through their network of partner banks.

Varo Bank: The High-Yield Choice for Daily Spenders

Varo is a “Neo-bank” designed for mobile users. They offer a 5.00% APY but require a $1,000 monthly direct deposit and a positive balance.

- The Standout Feature: No credit check and a highly intuitive app that helps you automate your savings every time you get paid.

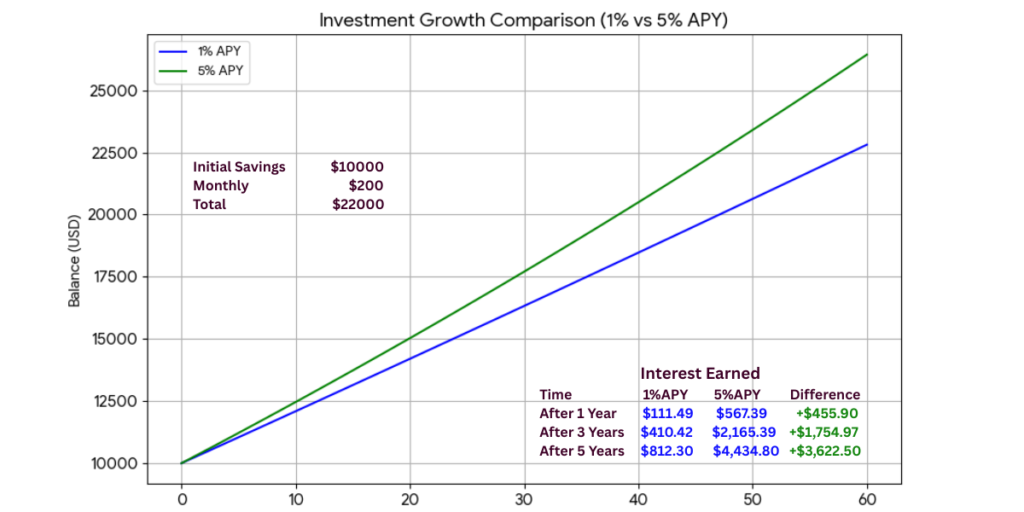

Your Savings Goal Calculator

Which Account Should You Open Today?

- If you want the absolute highest rate: Open an account with Digital Federal Credit Union (5.25% APY).

- If you want a simple, no-fuss high rate: Go with Bask Bank (5.10% APY).

- If you want to move your entire paycheck: Switch to SoFi.

Next Step: Once you’ve opened your account, link it to your primary checking and set up an “Auto-Save” of just $50 a week. By this time next year, you’ll have $2,600 plus interest—completely on autopilot.

Frequently Asked Questions: Best High-Yield Savings Accounts 2026

Are high-yield savings accounts FDIC insured?

Yes, all recommended accounts are FDIC-insured up to $250,000 per depositor, per bank (or NCUA insured for credit unions). Your money is protected even if the bank fails.

Will high-yield savings rates drop in 2026?

Possibly – rates track Fed funds (currently 4.25-4.50%). But even at 3.5% APY, you’d still earn 7x more than Chase/Wells Fargo’s 0.01-0.46%.

Is high-yield savings interest taxable?

Yes, all interest counts as ordinary income (reported on 1099-INT). Use a Roth IRA ladder for tax-free growth.

Is there a minimum deposit required?

Most have $0 minimums (Ally, Marcus) or $100 (SoFi). Perfect for emergency funds starting small.

Are there any withdrawal limits?

Federal Regulation D lifted – unlimited withdrawals. But 6/month “courtesy limit” common for transfers.

Are high-yield saving accounts suitable for beginners?

Yes! No credit check, instant online signup, mobile deposit checks. Start earning Day 1 vs 0.01% at big banks.

Park your cash smarter: Pick 1–2 accounts + subscribe to our newsletter for more savings tips.

What’s your savings goal? Comment!

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.