Student Loan Repayment in 2026: Navigating the New Rules

If you are repaying student loans in 2026, you are navigating a landscape that looks radically different than it did just a few years ago. Major regulatory shifts have fundamentally altered the math of federal repayment, making old strategies obsolete. To win in 2026, you must understand the new rules of engagement.

The core battle is now between maximizing federal protections (like the dominant SAVE plan) versus chasing a lower interest rate through private refinancing. This guide on student loan repayment in 2026 cuts through the noise to help you execute the correct strategy for your debt.

The Federal Solution: Mastering the SAVE Plan

As of March 2026, the **Saving on a Valuable Education (SAVE) plan** is the primary income-driven repayment (IDR) option for federal loan borrowers. The math behind SAVE is revolutionary because it is designed to prevent your balance from growing due to unpaid interest.

- The Core SAVE Rule: The SAVE plan calculates your payment based on just 5% of your discretionary income for undergraduate loans.

- The Interest Freeze Strategy: If your calculated SAVE payment is $0 (or less than the accruing interest), the government eliminates the remaining interest. This means that as long as you make your required payment, your total balance will not increase. This is a game-changer for financial stability.

Before making any changes, you must always check your specific loan details on the official StudentAid.gov portal. Knowing your loan types (Direct vs. FFEL) is critical for determining SAVE eligibility.

The Refinancing Decision: When to Go Private

While federal plans focus on safety and affordability, **Student Loan Refinancing** focuses on math and efficiency. This strategy involves taking out a new loan with a private lender to pay off your existing federal or private student loans.

The goal is to trade your current rates for a single, lower fixed interest rate. However, switching to a private loan is a “one-way street” that means you permanently lose access to federal benefits like forgiveness programs, income-driven repayment, and deferment options.

| Feature | Federal Loan (SAVE Plan) | Private Refinancing Loan |

|---|---|---|

| Interest Basis | Fixed (often higher) | Fixed (aiming for lower) |

| Payment Calculation | Income-driven (affordability focus) | Balance-driven (payoff focus) |

| Subsidized Interest | Yes (via SAVE) | No |

| Forgiveness Access | Yes (PSLF, IDR 20/25 year) | No |

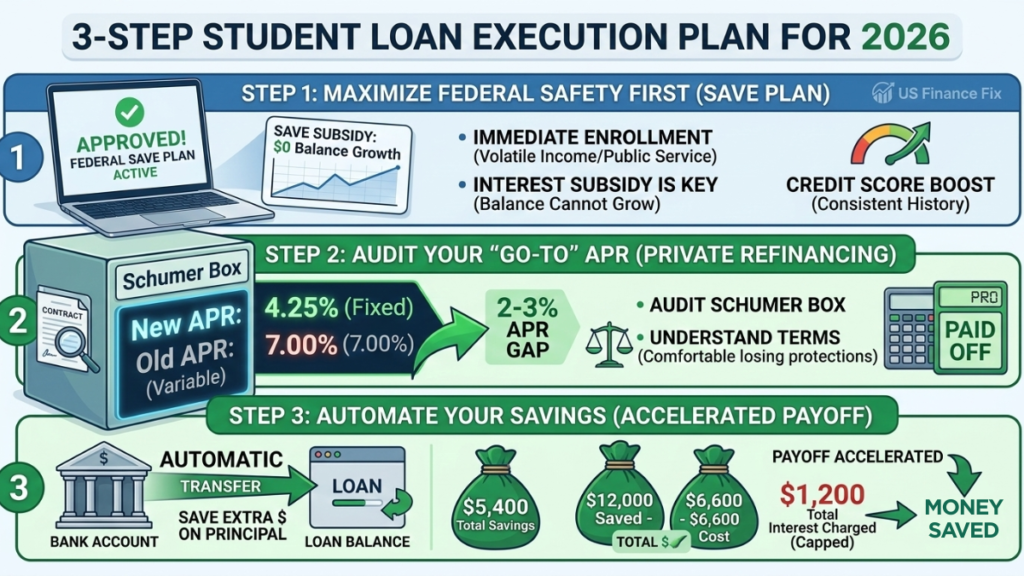

Alex’s 3-Step Execution Plan for 2026

- Maximize Federal Safety First: If your income is volatile or you work in public service, get on the SAVE plan immediately. The interest subsidy is too valuable to ignore. If your primary goal is building credit, the structured payments of SAVE can provide the consistent payment history needed for a boost to your credit score.

- Audit Your “Go-To” APR: If you are comfortable losing federal protections, you must audit the “Schumer Box” of private lenders. You want a 2–3% gap between your current average rate and the new refinancing rate. A clear understanding of the lender’s terms is vital here.

- Automate your Savings: If refinancing drops your rate from 7% to 4%, do not change your payment amount. Apply that “found money” directly to the principal to accelerate your payoff date, similar to how we structure a personal loan payoff strategy.

Student Loan Repayment in 2026: FAQs

What is the SAVE Plan interest subsidy?

This is the rule that stops your federal loan balance from growing. If your monthly interest charge is $100, but your income-driven payment on SAVE is only $30, the government covers (subsidizes) the remaining $70. Your balance will not increase by $70 that month.

Can I switch from a private student loan back to a federal loan?

No. Once you refinance a federal loan into a private loan, you lose all federal protections and benefits permanently. It is a one-way street.

Do student loans affect my credit score?

Yes. They are dynamic tradelines that impact your payment history, average age of credit, and credit mix. Consistent, on-time payments are essential, which is why monitoring tools like Chase Credit Journey are useful for beginners.

What happens if I miss a student loan repayment in 2026?

Missed payments are reported to credit bureaus, severely damaging your score and making it difficult to qualify for other products, like the best beginner travel credit cards. For federal loans, extended delinquency can lead to wage garnishment and tax refund offset.

Is PSLF still active in 2026?

Yes, the Public Service Loan Forgiveness (PSLF) program remains a critical federal benefit in 2026. It allows qualifying non-profit and government employees to have their remaining direct loan balance forgiven tax-free after 10 years of on-time payments. This benefit is lost if you refinance privately.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.