Personal Loans vs Credit Card Refinancing: When to Switch?

If you are carrying a balance on your credit cards in 2026, you aren’t just fighting a debt problem—you’re fighting a math problem. With average credit card APRs hovering at 24%, the “revolving” nature of the debt means your interest compounds daily, making it nearly impossible to see the finish line.

The solution for many is a Structural Debt Fix: swapping high-interest credit card debt for a fixed-rate personal loan. But is the switch always worth it? Let’s break down the math of a 12% personal loan versus a 24% credit card APR.

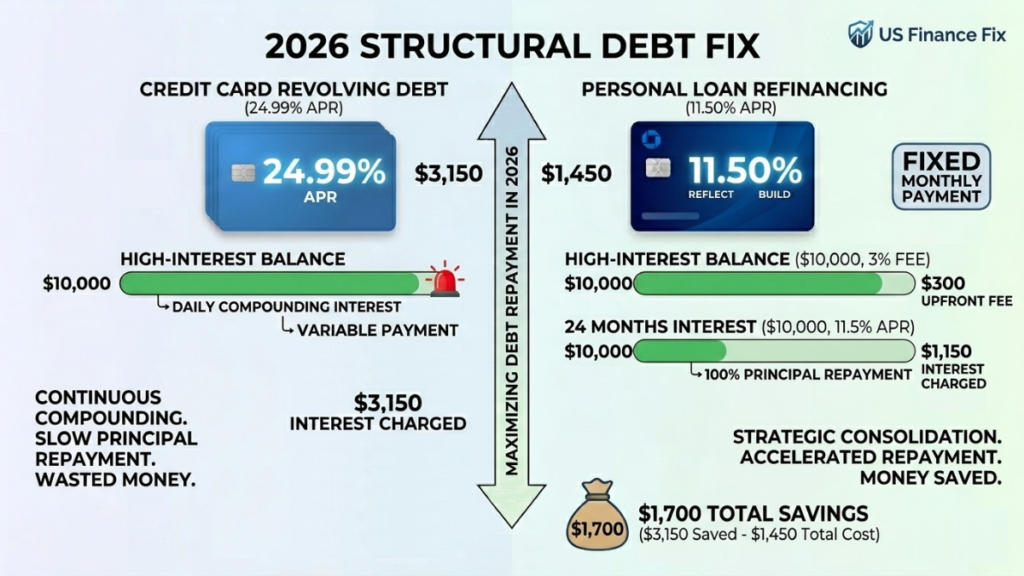

The Math: 24% Revolving vs. 12% Installment

The biggest difference between these two isn’t just the interest rate—it’s how the debt is structured. Credit cards are “revolving,” meaning your minimum payment drops as your balance drops, which actually keeps you in debt longer. A personal loan is an “installment” product with a fixed end date.

| Feature | Credit Card Debt | Personal Loan |

|---|---|---|

| Average APR | 24.99% (Variable) | 11.50% (Fixed) |

| Payment Structure | Revolving (Minimums change) | Installment (Fixed monthly) |

| Debt Payoff Date | Often 15-25 years | Defined (3-5 years) |

3 Signs It’s Time to Switch to a Personal Loan

- Your Credit Utilization is over 50%: Moving credit card debt to a personal loan shifts it from “revolving” to “installment” credit. This can trigger a massive boost to your credit score by instantly lowering your credit utilization ratio.

- You Have a Plan to Stop Spending: A personal loan only works if you don’t run up the credit card balances again. If you haven’t addressed the root cause of the debt, you’ll end up with a loan payment and new credit card bills.

- The APR Gap is at least 5%: To account for loan origination fees (typically 1-6%), you generally want your new loan’s interest rate to be at least 5 percentage points lower than your current cards.

Alex’s Pro-Tip: Before signing for a personal loan, always check the fine print for origination fees. If a lender charges a 5% fee upfront, that’s $500 out of a $10,000 loan that never hits your credit card balance.

Where to Find Refinancing Loans in 2026

For most beginners, the best rates are found through online lenders or credit unions. You can check your rate without a hard credit pull on platforms like SoFi or Upstart. For those with a lower score, our guide on best debt consolidation loans offers options for rebuilding credit.

Personal Loans vs Credit Card Refinancing: FAQs

Will a personal loan hurt my credit score?

You may see a temporary 5-10 point dip from the “Hard Inquiry” during the final application. However, most users see their score jump by 30+ points within 60 days because their credit utilization drops to zero on their credit cards.

What is an origination fee?

It is a one-time processing fee taken out of the loan proceeds. If you are approved for $10,000 with a 5% fee, you will receive $9,500 in your bank account, but you will owe back the full $10,000 plus interest.

Can I pay off a personal loan early?

In 2026, most reputable lenders do not charge “prepayment penalties.” We recommend only using lenders that allow you to pay extra toward your principal at any time without a fee.

What happens if I get denied for a loan?

If your score is too low for a 12% loan, don’t panic. You might need to focus on building your credit from scratch for 3-6 months to qualify for a better rate later.

Is a balance transfer card better than a personal loan?

A 0% APR balance transfer is better if you can pay the debt off in 18-21 months. A personal loan is better if you need a longer runway (3-5 years) to pay off a larger amount of debt.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.