How to Use Credit Karma to Boost Your Score Effectively (2026 Guide)

If you are staring at your dashboard and wondering how to move the needle, you’re not alone. In 2026, Credit Karma is more than just a score tracker;,it is a suite of credit-building tools. However, most users only check their “VantageScore” and leave. To actually boost your score, you need to use the platform’s “hidden” features to fix errors and optimize your utilization.

If you’re ready to start monitoring right now, you can sign up for Credit Karma for free.

1. Use the “Direct Dispute” Feature for Fast Wins

One of the most effective ways to see a jump in your score is to remove inaccuracies. Credit Karma has a Direct Dispute tool integrated with TransUnion. Instead of mailing letters, you can dispute errors directly in the app.

- What to look for: Late payments that you actually paid on time, accounts you didn’t open, or incorrect balances.

- The Impact: Removing one “wrongful” late payment can often result in a 20–50 point boost within 30 days.

2. Master the “Credit Utilization” Cheat Code

Your Credit Utilization Ratio accounts for roughly 30% of your score. Credit Karma shows you this percentage front and center. In 2026, “staying under 30%” is no longer the goal; staying under 10% is where the real score growth happens.

Alex’s Pro Tip: Use the “Credit Score Simulator” in the app to see exactly how much your score will rise if you pay off a specific card balance. It is surprisingly accurate.

3. Activate “Credit Spark™” for Alternative Data

If you have a “thin file” (few credit accounts), you can now use Credit Karma’s Credit Spark™ tool to report alternative data. This allows you to get credit for bills you are already paying, such as:

- Utility Bills (Electric, Water, Gas)

- Mobile Phone Plans

- Rent Payments

By reporting these to TransUnion, you build a positive payment history without taking on new debt.

4. Time Your Payments with “Statement Close Dates”

Credit Karma updates your info every 7 days, but your banks only report to the bureaus once a month. Look at the “Last Updated” date on your individual card details in Credit Karma. To maximize your boost, pay your balance 3 days before that date. This ensures a $0 or low balance is reported to the bureaus, instantly lowering your utilization.

5. Use the “Credit Builder” Account (If Eligible)

If your score is below 619, look for the Credit Karma Money™ Credit Builder. It’s a no-fee way to build payment history. You save as little as $10 per paycheck into a locked account, they report it as a “on-time loan payment,” and you get your money back once you hit $500. It’s a win-win for your savings and your score.

Credit Karma Limitations

- Missing Experian Data: It only monitors TransUnion and Equifax. Since many lenders (especially for credit cards and personal loans) only pull Experian, you could have a major inquiry or fraud event happen without receiving an alert.

- VantageScore Model: Like Chase, it uses VantageScore 3.0. This is often higher or lower than the FICO scores used by 90% of lenders, which can lead to “score shock” when you apply for a mortgage or car loan.

- No Identity Insurance: Unlike Chase Credit Journey, Credit Karma does not offer free identity theft insurance. If your identity is stolen, you are responsible for all legal and recovery costs out of pocket.

- Heavy Monetization: The platform is built on “Recommendations.” You will be constantly prompted to apply for credit cards and loans that the algorithm suggests, which can be distracting if you are trying to reduce debt.

Maximize your protection: “While Credit Karma is great for tracking two bureaus, it lacks built-in insurance. If you want a free safety net, you should also set up Chase Credit Journey. It’s one of the only free tools that includes $1 million in identity theft insurance for $0.”

How to Use Credit Karma to Boost Your Score: Frequently Asked Questions

Is the Credit Karma score accurate?

Yes, but it uses the VantageScore 3.0 model from TransUnion and Equifax. While this is a real credit score, most mortgage and auto lenders still use the FICO model. You might see a 15–40 point difference between the two, so use Credit Karma as a “trend tracker” rather than an absolute number.

How often does Credit Karma update?

Credit Karma typically updates your data every 7 days. However, if you have a major change (like a new hard inquiry or a significantly lower balance), you can sometimes trigger an “instant refresh” by logging in or checking your “Credit Monitoring” tab.

Why did my score drop after paying off a loan?

This is a common frustration. When you pay off a loan (like an auto or student loan), that account is marked as “Closed.” This can lower your average age of accounts or reduce your credit mix. Don’t panic; your score usually recovers within 2–3 months as your lower debt-to-income ratio is recognized.

Does checking Credit Karma hurt my score?

No. Checking your own score on Credit Karma is a “Soft Inquiry.” You can check it every single day without losing a single point. Only “Hard Inquiries”—which happen when you actually apply for a new credit card or loan—will impact your score.

Can I really remove late payments through Credit Karma?

You can use the Direct Dispute tool to challenge late payments that are inaccurate or unfair. If the bank cannot provide proof of the late payment within 30 days, it must be removed. However, if the late payment is accurate, the dispute will likely be denied unless you contact the lender directly for a “goodwill deletion.”

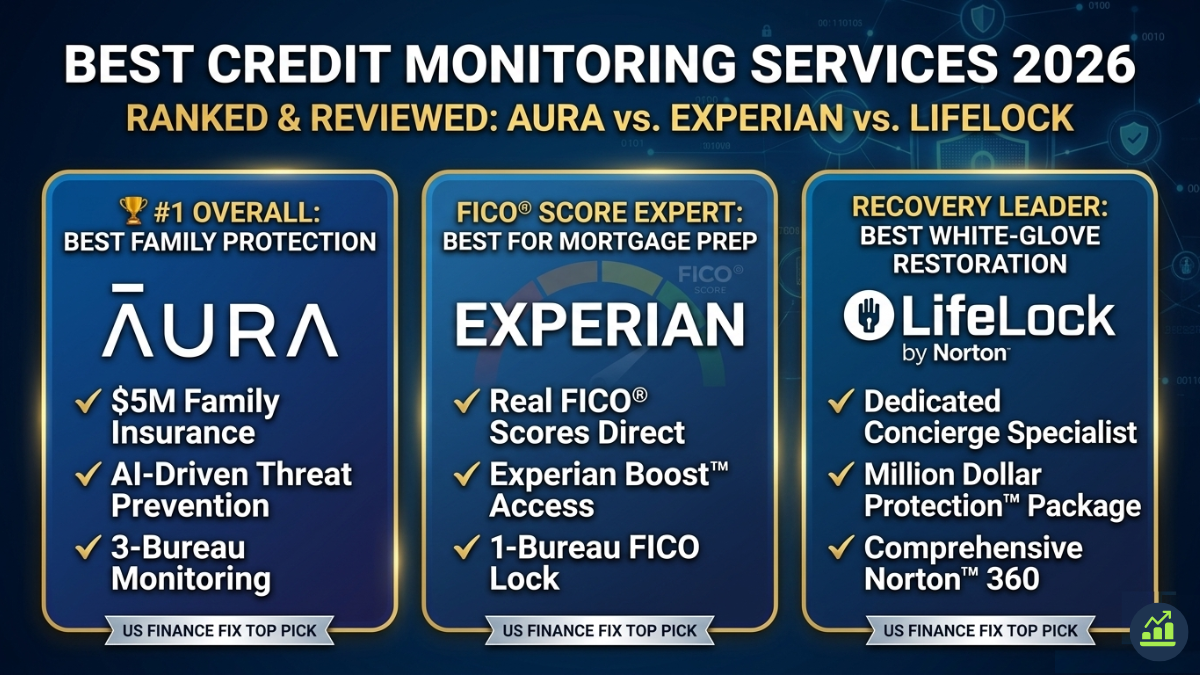

Ready to protect the score you’ve built? Before you leave, make sure you’ve compared the best credit monitoring services to ensure no one ruins your hard work with identity theft.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.