0% APR Balance Transfer Guide: The 2026 “Interest Freeze” Strategy

In 2026, the average credit card interest rate has hovered near 21%, making it feel nearly impossible to make a dent in your principal balance. If you are tired of watching your monthly payments disappear into interest charges, it’s time to deploy the “Interest Freeze” strategy.

By moving high-interest debt to a 0% introductory APR card, you effectively pause interest for up to 21 months, allowing 100% of your payment to hit the debt itself. Here is your tactical guide to mastering balance transfers this year.

What is the Interest Freeze Strategy?

The strategy is simple but requires precision: You apply for a specific credit card designed for balance transfers that offers a 0% APR for an introductory period (usually 15 to 21 months). Once approved, you “transfer” your existing high-interest balances to the new card. While you typically pay a one-time fee (3% to 5%), you save thousands in ongoing interest charges.

Best 0% APR Balance Transfer Cards for March 2026

As of March 2026, these are the top-tier “shovels” available to help you dig out of debt:

| Credit Card | Intro 0% Period | Transfer Fee | Apply |

|---|---|---|---|

| Wells Fargo Reflect® Card | 21 Months | 5% | Apply → |

| Citi Simplicity® Card | 21 Months | 3% (Intro offer) | Apply → |

| U.S. Bank Shield™ Visa® | 21 Months | 5% | Apply → |

| Chase Freedom Unlimited® | 15 Months | 3% (Intro offer) | Apply → |

The 4-Step Debt Payoff Execution

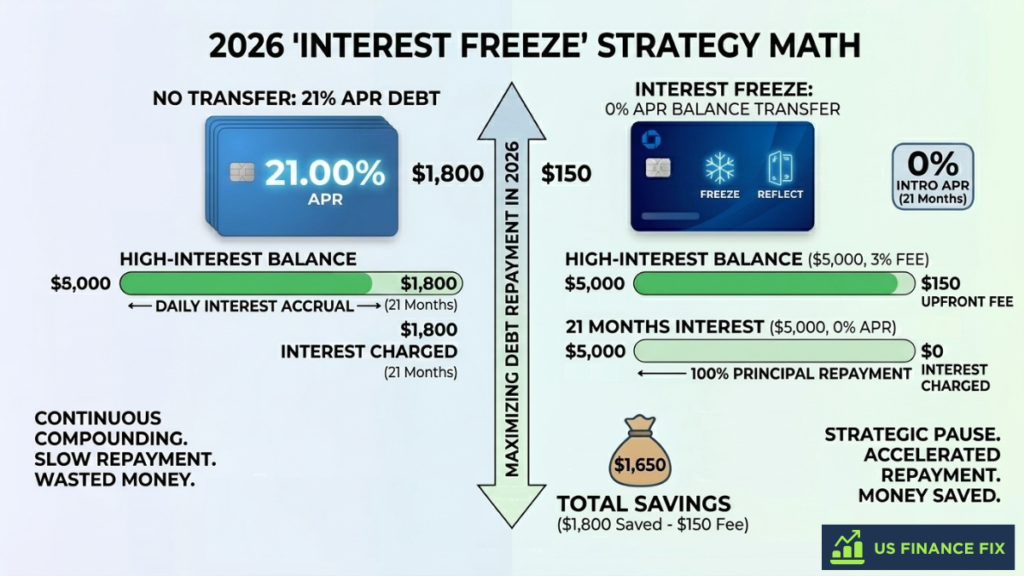

- The Math Check: Ensure the interest you’ll save over 18-21 months is significantly higher than the 3-5% transfer fee. (Example: A $5,000 transfer at a 5% fee costs $250, but saves ~$1,800 in interest at 21% APR).

- Apply for the “Runway”: Choose a card that gives you the longest runway. If you have $10,000 in debt, you want the full 21 months offered by cards like the Wells Fargo Reflect®.

- Request the Transfer: You can usually do this during the application process or immediately after your account is opened. Note: Most banks require transfers to be requested within the first 60–120 days to get the 0% rate.

- Automate the Kill-Date: Divide your total balance by the number of 0% months (minus one for safety). If you owe $4,000 on a 21-month card, aim to pay $200/month to be debt-free before the “Interest Freeze” thaws.

Alex’s Pro-Tip: Never use your balance transfer card for new purchases. Adding new debt to a card you are trying to pay off complicates the math and can lead to “double-dipping” on interest if you miss the grace period. Use a dedicated everyday spending card for your necessities to earn rewards while your old debt stays frozen at 0%.

0% APR Balance Transfer Guide: FAQs

Does a balance transfer hurt my credit score?

Initially, you may see a small dip due to the “Hard Inquiry” from the application. However, your score typically improves quickly because you are increasing your total available credit, which lowers your Credit Utilization Ratio.

Can I transfer a balance between two cards from the same bank?

Generally, no. For example, you cannot transfer debt from a Chase Sapphire to a Chase Freedom. Banks use these offers to “steal” customers from competitors, not to help you pay less interest on debt they already own.

What happens if I don’t pay off the balance before the 0% ends?

Once the introductory period ends, the remaining balance will be hit with the standard variable APR (often 18% to 29%). Unlike “Deferred Interest” store cards, you usually aren’t charged retroactive interest—only interest on the remaining amount moving forward.

Can I do multiple balance transfers to the same card?

Yes, as long as you stay within your total credit limit and perform the transfers within the bank’s allowed promotional window (usually the first 2-4 months).

Should I close my old credit card after the transfer?

In most cases, keep the old card open with a $0 balance. Closing it could shorten your “Age of Credit” and increase your utilization, potentially hurting your credit score. Just hide the card in a drawer so you aren’t tempted to spend on it again!

Before applying for a new line of credit, ensure your report is accurate by using a top-tier credit monitoring service to catch any errors that might lower your approval odds.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.