How to Calculate Your Credit Utilization Ratio (And Why the ‘30% Rule’ is Wrong)

If you’ve ever looked up how to improve your credit score, you’ve likely heard the “30% Rule” – the idea that as long as you keep your balances below 30% of your limit, your score is safe. Is that the right way to calculate credit utilization ratio?

I’m Alex Hale, and I’m here to tell you that the 30% rule is a myth. While 30% is better than 90%, it is still considered “high” by the most sensitive FICO algorithms. If you want a top-tier score, you need to understand the real math behind utilization.

The Step-by-Step Math to Calculate Credit Utilization Ratio

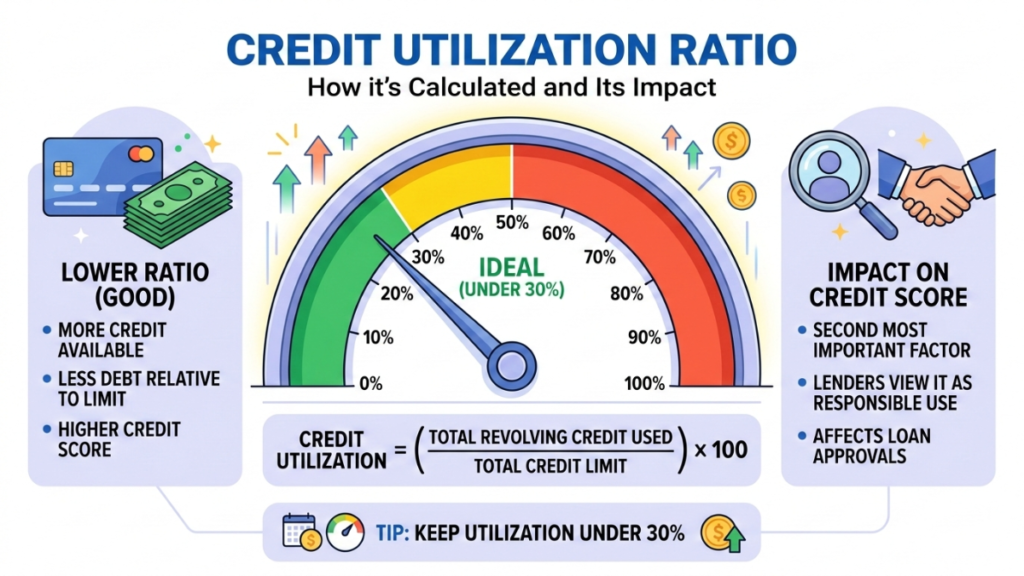

Your Credit Utilization Ratio is calculated by dividing your total credit card balances by your total credit limits. The formula looks like this:

{Utilization} = ({Total Balances}/{Total Limits}) times 100Example: If you have a total credit limit of $10,000 across all cards and your current statement shows a balance of $3,000, your utilization is exactly 30%.

Why the ‘30% Rule’ is Failing You

Credit scoring models like FICO and VantageScore view utilization on a sliding scale. There isn’t a “magic cliff” at 30%. Instead, your score improves as your utilization drops into lower brackets:

- 30% – 49%: “Fair” – You aren’t hurting your score badly, but you aren’t helping it.

- 10% – 29%: “Good” – You will see a noticeable bump in your score.

- 1% – 9%: “Exceptional” – This is the sweet spot where the highest scores live.

- 0%: “Excellent” – But be careful. Sometimes a tiny balance (1%) is better than 0% to show “activity.”

The Alex Hale “Power User” Move

The biggest mistake people make is paying their bill on the Due Date. By then, the bank has already reported your high balance to the credit bureaus.

The Fix: Find your “Statement Closing Date” (usually 21-25 days before your due date) and pay your balance down to 1-5% BEFORE that day. This forces the bank to report a low utilization, even if you spend a lot during the month.

Frequently Asked Questions

Does utilization have a memory?

No. Unlike late payments, credit utilization “resets” every month. If you have 90% utilization this month and pay it down to 5% next month, your score will bounce back almost immediately once the new balance is reported.

Is 0% utilization better than 1%?

Technically, having 1% reported shows you are using your credit responsibly. A string of 0% reports can sometimes lead the algorithm to think the card is inactive.

Should I spread my debt across multiple cards?

FICO looks at both aggregate utilization (all cards combined) and individual utilization (each card). If one card is maxed out, it will hurt your score even if your total utilization is low.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.