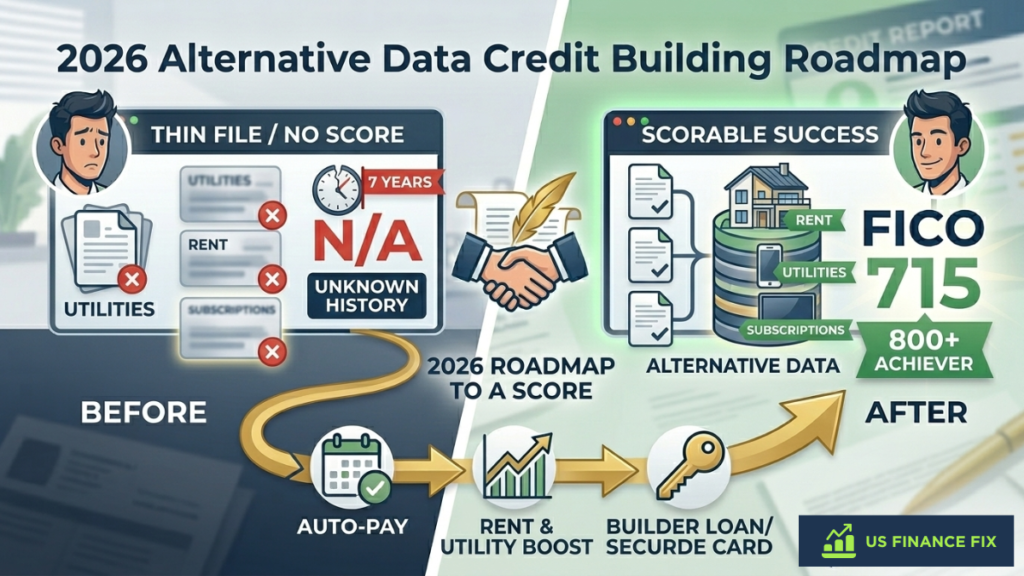

Building Credit from Scratch in 2026: The “Alternative Data” Roadmap

The New Reality: In 2026, you no longer need a credit card to build a credit score. Thanks to “Alternative Data,” your rent, phone bill, and even your Netflix subscription can now act as the foundation for an elite score.

Whether you are a Gen Z’er starting fresh or an immigrant new to the US financial system, the “Thin File” struggle is real. Banks won’t give you credit because you don’t have a score, but you can’t get a score without credit. This guide on building credit from scratch breaks that cycle using the latest 2026 reporting tools.

1. Activate the “Invisible” History: Experian Boost™

The fastest way to go from “No Score” to “Scorable” in 2026 is by reporting the bills you already pay. Tools like Experian Boost allow you to link your bank account to your credit file.

- What it counts: Cell phone plans, utilities, and streaming services (Netflix, Disney+, etc.).

- The Benefit: These on-time payments are added to your Experian file instantly, often resulting in a 10–15 point jump for thin files.

2. The Rent Reporting Revolution

For decades, your biggest monthly expense—rent—did nothing for your credit. In 2026, services like Rental Kharma or RentTrack (and even some landlord-specific portals) allow you to report your past 24 months of rent history. This adds “Age of Accounts” to your report, which is a massive 15% of your total score.

Alex’s 2026 Growth Hack

If you’re starting at zero, look for a Credit Builder Loan (like those from Self or your local credit union). Unlike a traditional loan, you don’t get the money upfront. You pay into a locked savings account, and the bank reports those payments as “Installment Debt.” At the end, you get your money back AND a established credit history.

3. The “Secured” Stepping Stone

Once you have used alternative data to hit a 600+ score, it’s time for a Secured Credit Card. These cards require a deposit (usually $200), which becomes your limit. In 2026, the best secured cards—like the Discover it® Secured—automatically graduate to “Unsecured” after 6–7 months of responsible use, returning your deposit.

If you are ready to take this step, check out our curated list of the best credit cards for rebuilding credit to find a lender that specializes in ‘thin-file’ or ‘rebuilding’ profiles.

Building Credit from Scratch: FAQs

How long does it take to get a credit score from zero?

If you use the 2026 alternative data methods, you can often generate a VantageScore within 30 days. However, a FICO score (which most lenders prefer) usually requires at least 6 months of reporting history on an account.

Do “Buy Now, Pay Later” (BNPL) services help my credit?

As of 2026, most BNPL services (like Affirm and Klarna) have begun reporting to the major bureaus. While they can help build history, be careful: many small, short-term loans can make your report look “cluttered” to mortgage lenders.

Can I build credit by using a Debit Card?

Generally, no. Standard debit cards do not report to bureaus. However, new “Credit-Builder Debit” cards (like Fizz or Chime) now exist that feel like debit but report as credit. These are excellent for those who want to avoid debt while building a score.

Ready to Graduate to Rewards?

Once you hit a 670 score, you’re ready for the big leagues. Check out our guide on the best cards for daily spending. Best Credit Cards 2026

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.