Best Everyday Spending Credit Cards 2026: Maximizing Every Dollar

The 2026 Reality: With grocery and gas prices stabilizing at higher levels, a generic 1% card is no longer enough. To stay ahead, your wallet needs a strategy that specifically targets High-Frequency spending – the stuff you buy every single Tuesday.

Most Americans lose over $500 a year simply by using the “wrong” card at the grocery store or gas pump. In 2026, the market has shifted toward “Lifestyle Tiering,” where banks reward your daily habits more than your occasional travel. This guide on best everyday spending credit cards breaks down the top picks to ensure no dollar is left on the table.

At a Glance: The 2026 Everyday Spend Strategy

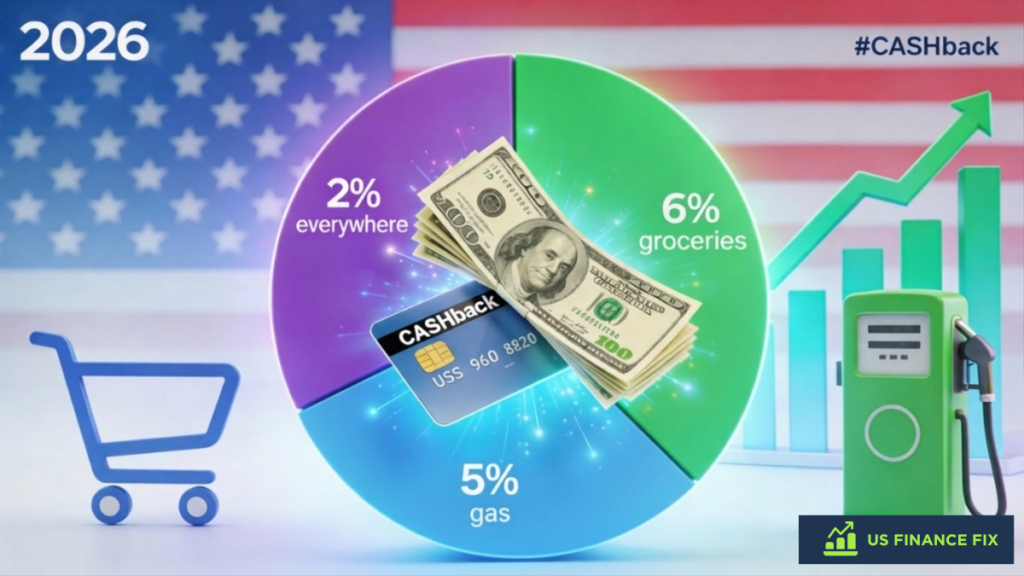

- Best for Families: Amex Blue Cash Preferred® (6% back on groceries/streaming).

- Best for Simplicity: Wells Fargo Active Cash® (Unlimited 2% back on everything).

- Best for Commuters: Citi Custom Cash® (Targeted 5% back on gas).

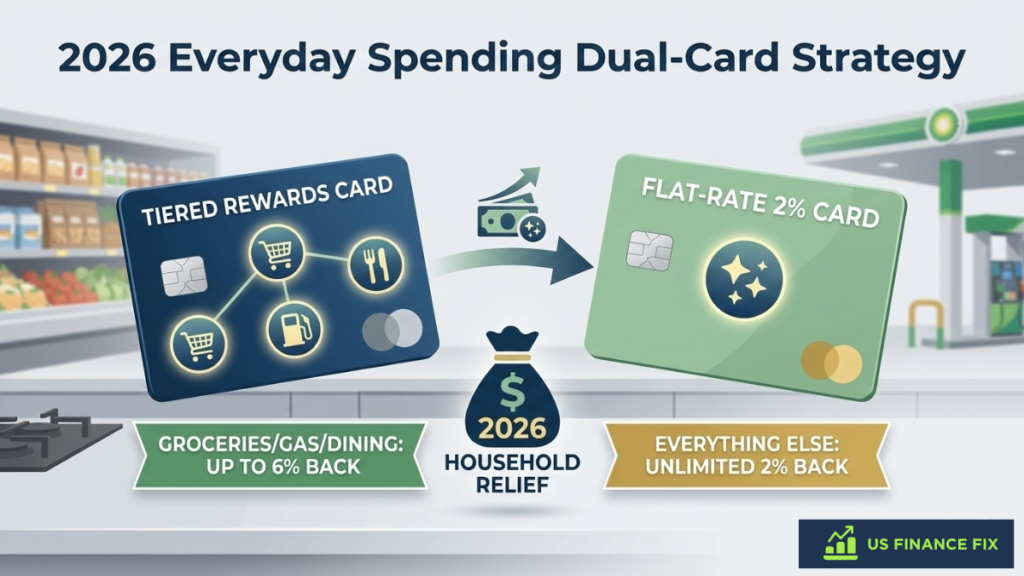

- The “Fix-It” Pro Tip: Use a 2-card system to ensure you never earn less than 2% on any purchase.

- The Warning: Most “6% Grocery” rewards exclude Walmart, Target, and Costco.

The “Daily Driver” Hierarchy: Top 3 Picks for 2026

| Card Name | Card Type | Best For… | Top Reward Rate | Annual Fee |

|---|---|---|---|---|

| Amex Blue Cash Preferred® | The Grocery Giant | Supermarkets & Streaming | 6% Cash Back | $0 first year, then $95 |

| Citi Custom Cash® | The Commuter King | Gas & EV Charging | 5% Cash Back | $0 |

| Wells Fargo Active Cash® | The Flat-Rate Hero | Everything Else | 2% Unlimited | $0 |

1. Blue Cash Preferred® from American Express

This remains the undisputed heavyweight for US households. If you spend $100+ a week on groceries, this card pays for itself within months.

- 6% Cash Back at U.S. supermarkets (on up to $6,000 per year in purchases, then 1%).

- 6% Cash Back on select U.S. streaming subscriptions.

- 3% Cash Back at U.S. gas stations and on transit.

- Apply here

Alex’s 2026 Tip: Remember to always read the Schumer Box. The 6% supermarket cash-back does NOT apply to Walmart or Target. Use your 2% flat-rate card there instead.

2. Wells Fargo Active Cash® Card

For those who hate tracking categories, this is the “set it and forget it” champion for 2026.

- Earn unlimited 2% cash rewards on purchases.

- $0 Annual Fee.

- Cell Phone Protection: Get up to $600 of protection against damage or theft (subject to a $25 deductible).

- Apply here

3. Citi Custom Cash® Card

This card is unique because it automatically adapts to your spending. It gives you 5% back on your top spending category each billing cycle (up to $500 spent).

- 5% back on categories like Dining, Gas, or Groceries.

- No rotating categories to sign up for. The card does the math for you.

- Apply here

The Alex Hale “Fix-It” Verdict

Don’t try to juggle five cards. For 90% of US consumers, the “Dual-Card System” is the sweet spot. Use a Tiered Rewards Card (like the Amex Blue Cash) for your groceries and gas, and a Flat-Rate Card (like the Wells Fargo Active Cash) for everything else. This ensures you never earn less than 2% on any purchase you make in 2026.

The 2026 Everyday Rewards Calculator

| Monthly Spend Category | Estimated Spend | Standard Card (1%) | Everyday Duo (Average 4%) | Annual “Fix-It” Bonus |

| Groceries | $600 | $6.00 | $36.00 | $360.00 |

| Gas / Transit | $250 | $2.50 | $12.50 | $120.00 |

| Dining / Apps | $300 | $3.00 | $9.00 | $72.00 |

| Misc. / Utilities | $850 | $8.50 | $17.00 | $102.00 |

| TOTALS | $2,000/mo | $20/mo | $74.50/mo | $654 / year |

Best Everyday Spending Credit Cards: 2026 FAQ

1. Does “Grocery” cash back include spending at Walmart, Target, or Costco?

Generally, no. Most major issuers (like Amex and Chase) classify Walmart and Target as “Superstores” or “Discount Stores” rather than “Supermarkets.” Similarly, Costco and Sam’s Club are classified as “Wholesale Clubs.” To earn the highest rewards at these locations, you should use a flat-rate 2% card or a card specifically branded for that store.

2. How many credit cards do I actually need for everyday spending?

For the average US household, a “Dual-Card System” is the sweet spot. This involves one Tiered Rewards Card (earning 3–6% on groceries and gas) and one Flat-Rate Card (earning 2% on everything else). This setup maximizes your rewards without the headache of managing 5+ different payment dates and apps.

3. Is it better to earn Points or Cash Back for daily expenses?

In 2026, cash back is the preferred choice for everyday spending because of its “Guaranteed Value.” While travel points can offer higher ceilings, they require time-consuming optimization. Cash back provides immediate “Household Relief” by reducing your monthly bills automatically through statement credits.

4. Will my rewards be devalued in 2026?

While some luxury travel perks are seeing devaluations, standard cash-back rates (like 2% flat or 6% grocery) have remained stable. Card issuers are currently competing heavily for “daily spend” volume, making 2026 an excellent year to lock in a high-rate everyday card.

5. How can I easily track which card to use for which purchase?

The simplest method is the “Color Code” or “Sticker” trick. Place a small green sticker on your grocery card and a blue one on your “everything else” card. Alternatively, digital wallets like Apple Pay and Google Pay allow you to nickname your cards (e.g., “6% Grocery”) so you see the reward type right before you tap to pay.

6. Do I have to pay an annual fee to get good everyday rewards?

Not necessarily. While “Premium” cards like the Amex Blue Cash Preferred have a $95 annual fee, they often pay for themselves if your grocery spend exceeds $3,200 a year. If you spend less than that, a “No-Annual-Fee” card like the Wells Fargo Active Cash or Citi Custom Cash is often the mathematically superior choice.

Ready to Optimize Your Wallet?

Check out our full breakdown of the best cards for your specific credit score. View Best Credit Cards 2026

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.