Best Credit Cards for Rebuilding Credit in 2026: Repair Your Score Fast

Struggling with a FICO score under 600 or a “thin” credit file? In 2026, best credit cards for rebuilding credit are the single most effective tool to stop paying high interest on loans and start getting approved again. I’ve analyzed the latest approval trends for March 2026 to find 8 cards that build your score without predatory fees.

Alex’s Quick Win: If you have $200, get a Secured Card (Instant approval). If you have $0, look for Unsecured “Second Chance” Cards like Capital One Platinum. Both report to all 3 bureaus. Positive history builds score everywhere.

Secured vs. Unsecured: Which Should You Choose?

In 2026, the “Rebuild” market is split into two categories. Choosing the wrong one can cost you $100+ in unnecessary annual fees.

| Feature | Secured Cards | Unsecured Cards |

|---|---|---|

| Security Deposit | $49 – $500 (Refundable) | $0 |

| Approval Odds | 99% (Perfect for bad credit) | 65% (Best for “Fair” credit) |

| Upgrade Path | Refunds deposit in 6-12 months | N/A (Static limit) |

8 Best Credit Cards for Rebuilding Credit (2026 Comparison)

| Card Name | Annual Fee | Key Benefit | Best For |

|---|---|---|---|

| Capital One Platinum Secured | $0 | Deposit as low as $49 | The #1 Starter Card |

| Discover it® Secured | $0 | 2% Cash Back on Gas/Dining | Earning Rewards |

| Chime Credit Builder | $0 | No Credit Check | No upfront deposit |

| Chase Freedom Rise℠ | $0 | 1.5% Cash Back | Chase Ecosystem Entry |

| Mission Lane Visa® | $0 – $59 | Instant Credit Limit Boost | Unsecured Bad Credit |

| OpenSky® Secured Visa® | $35 | No Bank Account Required | Privacy/No Check |

| Petal® 2 Visa® | $0 | No Deposit / No Fees | Cash Flow Underwriting |

| Self Visa® Secured | $0* | Builds Savings + Credit | Total Beginners |

Top 3 Deep-Dives: Why These Win in 2026

1. Capital One Platinum Secured: The “No-Brainer” Entry Card

This remains my top recommendation for 2026 because it has the lowest barrier to entry in the industry.

- The Low-Deposit Secret: While most cards demand a 1:1 deposit (you pay $200 for a $200 limit), Capital One uses “partial funding.” Based on your credit, you might only need to put down $49 or $99 to get that same $200 line.

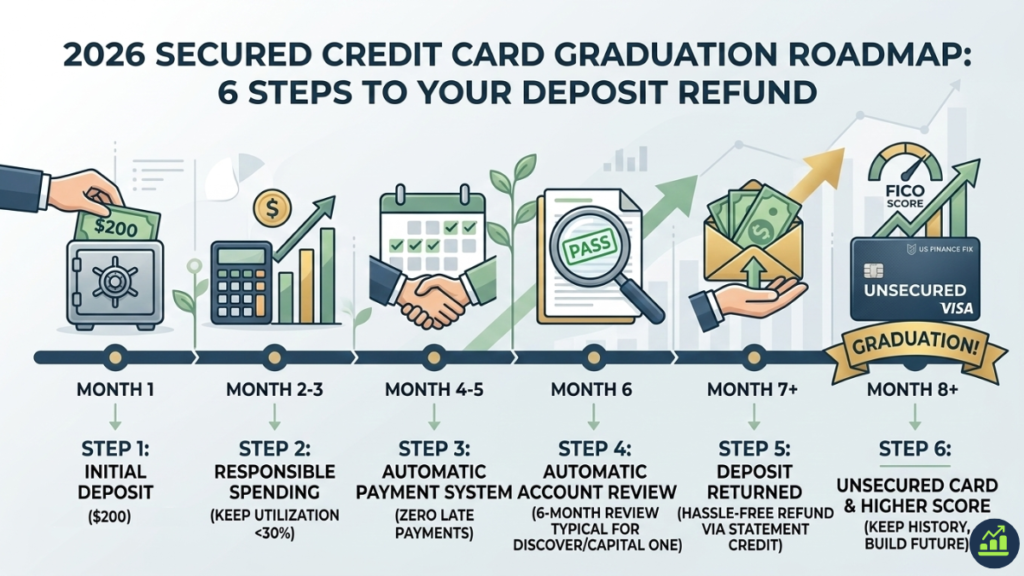

- The “Hassle-Free” Graduation: They are aggressive with automatic reviews. In 2026, most users report their deposit being returned as a statement credit in exactly 6 months of on-time payments.

- Best For: Those who are “cash-strapped” but want a big-name bank on their credit report.

- Apply here

2. Discover it® Secured: The Best Card You’ll Actually Keep

Discover is the only “rebuild” card that doesn’t feel like a “rebuild” card. It’s a legitimate rewards card that grows with you.

- The 2026 Double-Down: You earn 2% cash back at gas stations and restaurants (on up to $1,000 in combined purchases each quarter). At the end of your first year, Discover automatically matches all the cash back you’ve earned. If you earned $50, they give you $50 more.

- Path to Unsecured: Starting at 7 months, Discover begins monthly automatic reviews to transition you to the “unsecured” version. When you graduate, you keep your account history (great for your score) and get your $200+ deposit back.

- Best For: People who want to earn money while they fix their credit.

- Apply here

3. Chime Card™ (Formerly Credit Builder): The “Safety” Net

Chime changed the game by removing the two things people hate most: credit checks and fixed security deposits.

- How the “SDA” Works: When you move money into your Secured Deposit Account (SDA), that amount becomes your spendable limit. If you move $50, your limit is $50. It’s impossible to spend money you don’t have, meaning you can never go into debt.

- New for 2026: Chime+ members now earn 1.5% cash back on rotating categories (like groceries or utilities) when they have a qualifying direct deposit.

- The Utilization Hack: Chime does not report “Credit Utilization” to the bureaus because there is no pre-set limit. This is a massive win if you tend to carry a balance, as it prevents your score from dropping due to high usage.

- Best For: Those who have been denied elsewhere or are afraid of overspending.

- Apply here

3 Mistakes That Will Tank Your Rebuild

- Paying Only the Minimum: In 2026, APRs for rebuild cards average 29.99%. Paying interest will wipe out any credit score benefit.

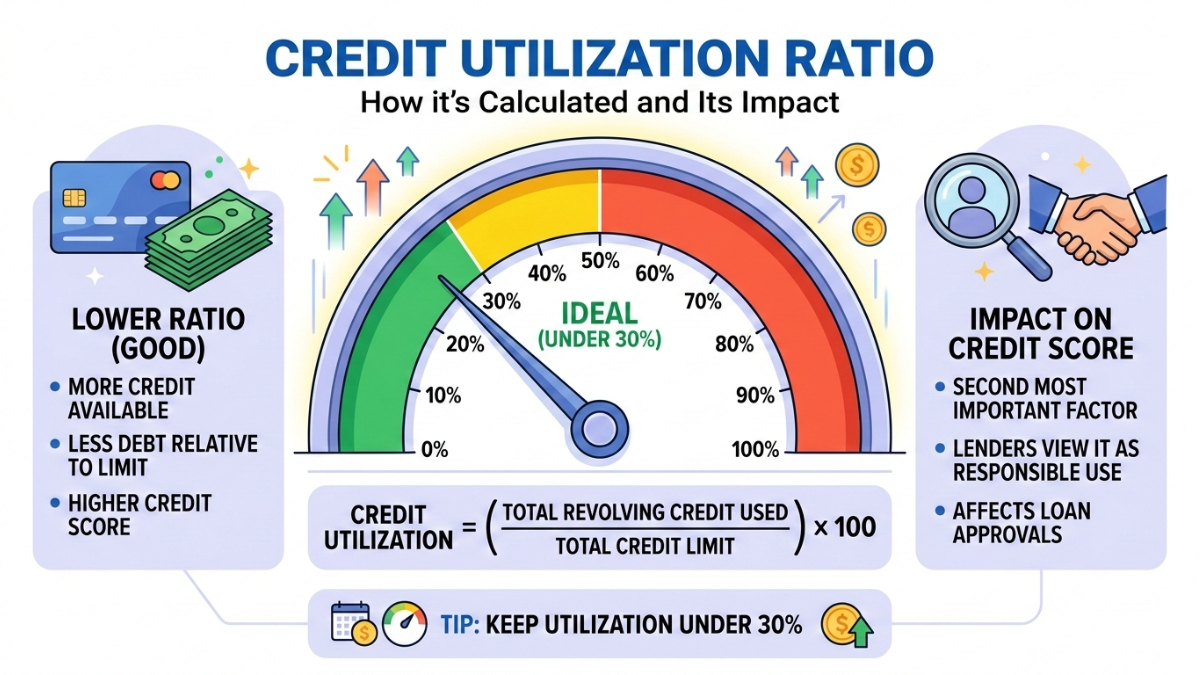

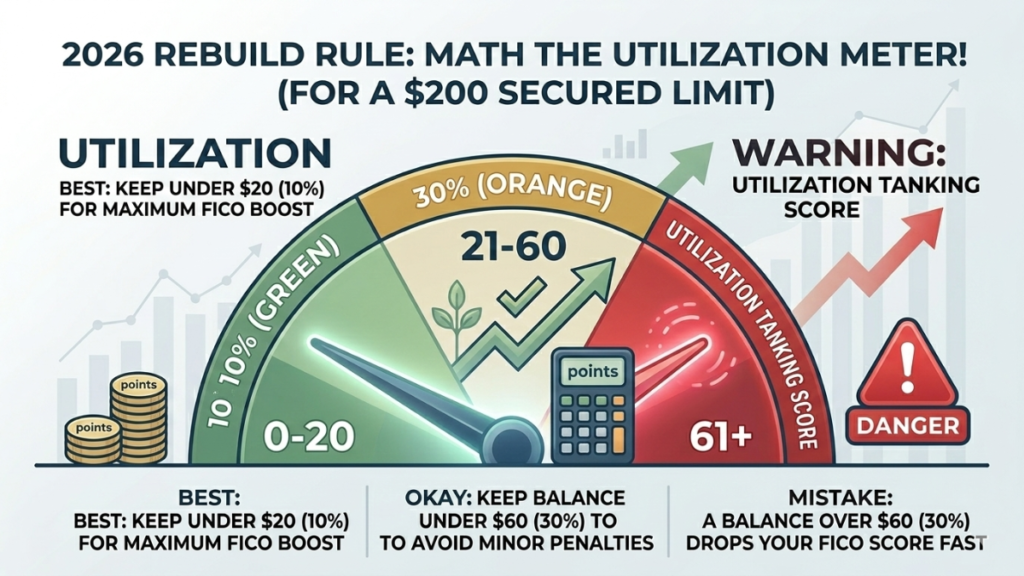

- High Utilization: If your limit is $200, never let your balance stay above $60 (30%). Ideally, keep it under $20 (10%).

- Applying for Too Many: Each “Hard Pull” can drop your score 5-10 points. Use Pre-Approval tools before hitting the final submit button.

Best Credit Cards for Rebuilding Credit: FAQs

How fast can I see my score go up?

Most users see a 30–60 point increase within the first 3 months of on-time payments. By month 6, many are eligible to “graduate” to a traditional unsecured card. If your score is stuck, check our Credit Utilization Guide to see if your balances are too high.

Can I rebuild my credit if I have a bankruptcy?

Yes. The Mission Lane Visa and OpenSky Secured are specifically known for approving applicants with discharged bankruptcies in 2026. Avoid applying for Chase or Amex until at least 2 years post-discharge.

Do I need a bank account to get these cards?

Not necessarily. The OpenSky® Secured Visa® allows you to fund your deposit via money order or Western Union, making it the best choice for the “unbanked.”

Should I close my secured card once my score is better?

No. Closing your oldest account can actually drop your score by reducing your “Average Age of Accounts.” Only close it if there is a high annual fee. Otherwise, ask the issuer to “product change” it to a no-fee cash back card.

Ready for the next level? Once your score hits 670+, you’re ready for our Travel Credit Cards for Beginners guide to start earning free flights.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.