Best Debt Consolidation Loans US in 2026 (Even If Your Credit Is Under 650)

High-interest credit card debt can feel like running on a treadmill that keeps getting faster. In 2026, with average credit card APRs hovering near 23%, debt consolidation isn’t just a convenience – it’s a survival strategy.

But what if your credit score isn’t “perfect”? If you’re sitting in the 580 to 640 range, many big banks will show you the door. Fortunately, a new wave of FinTech lenders uses AI and alternative data to look past just a three-digit number. Here is our expert breakdown of the best debt consolidation loans for “fair” to “bad” credit in 2026.

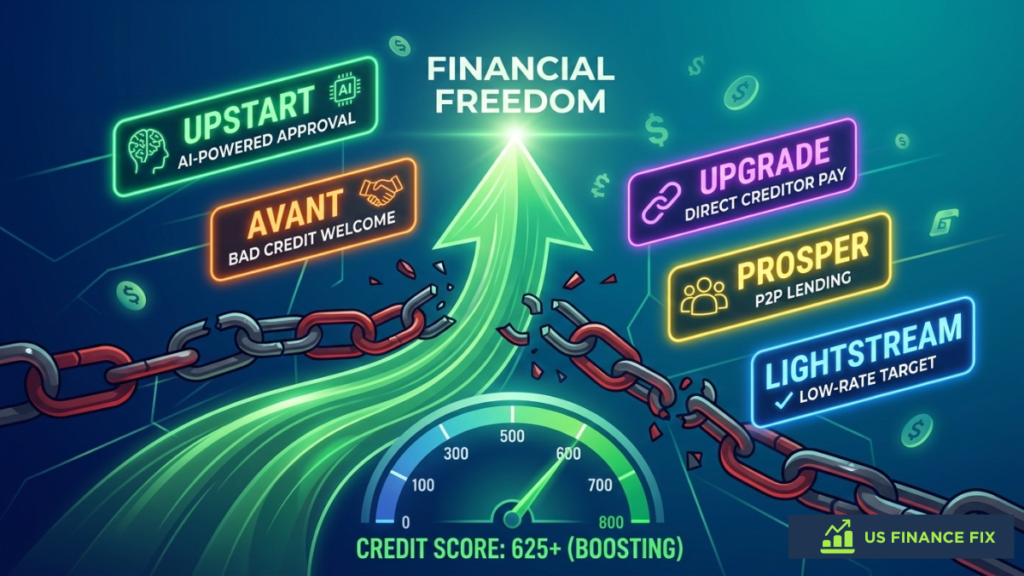

Best Debt Consolidation Loans 2026 Comparison: Top Lenders for Fair Credit

| Lender | Min. Credit Score | APR | Max Loan | Funding Speed | Best For… | Apply |

|---|---|---|---|---|---|---|

| Upstart | None / 580* | 7.8–35.99% | $50,000 | Next day | Thin credit history | Pre-qualify → |

| Upgrade | 580 | 9.95–35.99% | $50,000 | 1–2 days | Direct creditor payment | Apply → |

| Avant | 550 | 8.49–35.99% | $35,000 | Same day | Lower income earners | Apply → |

| Prosper | 640 | 8.99–35.99% | $50,000 | 3 days | Peer-to-Peer lending | Apply → |

| LightStream | 660+ | 6.99–25.99% | $100,000 | Same day | High income / Good credit | Apply → |

The Math of Consolidation: How Much Will You Actually Save?

At US Finance Fix, we believe a loan is only a “fix” if it puts money back in your pocket. Many people focus on the monthly payment amount, but the real victory is in the Total Interest Saved.

In 2026, the gap between credit card APRs and debt consolidation loans is wider than ever. Let’s look at a typical “US Finance Fix” scenario:

Scenario A: The Credit Card Treadmill

- Total Debt: $15,000

- Average Credit Card APR: 24%

- Monthly Interest Charge: ~$300

- The Problem: You are paying $3,600 a year just to “stay even” with your debt. None of that money is actually lowering your balance.

Scenario B: The 2026 Consolidation Fix

- Loan Amount: $15,000

- New Personal Loan APR: 12% (Average for scores near 620)

- Monthly Interest Charge: ~$150

- The Victory: You instantly save $150 per month ($1,800 per year) in interest alone.

Where Does That “Saved” $1,800 Go?

If you take that $150/month in savings and apply it as an extra payment toward your loan principal, you could potentially cut 18 months off a 5-year loan.

This is the true power of consolidation: it doesn’t just move your debt; it buys you time and lowers the total “cost of living” for your household. By reducing your interest, you also lower your Debt-to-Income (DTI) ratio, which is exactly what lenders like Upstart and Upgrade want to see before they offer you even better rates in the future.

Download our free debt consolidation calculator to calculate your potential savings.

1. Upstart: Best for “Non-Traditional” Profiles

Upstart is a 2026 leader because they don’t just look at your FICO. They use AI to consider your education and job history. If you have a decent job but a low score due to high credit utilization, Upstart is often the easiest to get approved with.

- Min. Credit Score: None / 580* (Uses AI to evaluate “thin” files).

- Loan Amounts: $1,000 – $50,000.

- Pros: Faster approval for “thin” credit than Prosper. Accepts applicants that LightStream would typically reject.

- Cons: Higher origination fees (up to 12%) compared to Upgrad. APRs can be steep if your DTI is high.

2. Upgrade: Best for Effortless Consolidation

Upgrade offers a “Direct Pay” feature where they send the loan funds directly to your credit card companies. This prevents you from accidentally spending the loan money on something else—a common pitfall in debt recovery.

- Min. Credit Score: 580.

- Loan Amounts: $1,000 – $50,000.

- Pros: Lower APRs than Avant for those with a 600+ score. “Direct Pay” feature is more convenient for debt-crushing than LightStream.

- Cons: Not available in all 50 states. Requires more documentation than the AI-driven Upstart model.

3. Avant: The Bad Credit Specialist

If your score is hovering near 550, Avant is your most likely path to approval. They specialize in the “middle-class” borrower who has hit a few bumps in the road but has stable income.

- Min. Credit Score: 550.

- Loan Amounts: $2,000 – $35,000.

- Pros: Most accessible lender on this list for “Bad Credit”. Faster funding than Prosper’s peer-to-peer model.

- Cons: The lowest loan ceiling ($35k) compared to LightStream’s $100k. Significantly higher interest rates than Upgrade.

4. Prosper: Best for Joint Applications

Prosper is a peer-to-peer (P2P) lending platform. In 2026, they remain a top choice for those with “Fair” credit who want a fixed-rate, predictable monthly payment and the option to add a co-borrower.

- Min. Credit Score: 640.

- Loan Amounts: $2,000 – $50,000.

- Pros: Allows co-applicants (unlike Upstart), which helps lower your rate. Fixed monthly payments are often more stable than Avant.

- Cons: Funding takes 3–5 days (slower than Upgrade’s next-day funding). Requires a higher minimum score than Avant.

5. LightStream: The “Reward” for Reaching 660

LightStream (a division of Truist) is the “Elite” lender on this list. They target consumers with established credit histories and reward them with the lowest rates in the industry.

We recommend LightStream as the “Target.” Once your credit repair efforts (using tools like Credit Karma to boost your score) get you above 660, LightStream becomes the best option. They charge zero fees and offer the lowest rates in the industry.

- Min. Credit Score: 660+ (700+ preferred).

- Loan Amounts: $5,000 – $100,000.

- Pros: Zero fees (no origination or late fees), making it much cheaper than Upstart. Higher loan limits than Upgrade or Avant.

- Cons: Hardest to qualify for. No “Direct Pay” to creditors like Upgrade, requiring you to handle the payouts yourself.

The 2026 Best Debt Consolidation Loans Decision Tree

If you are overwhelmed by the choices, use this quick guide to find the best debt consolidation loans:

- If your credit score is 550–600: Start with Avant. They are the most flexible with lower scores and offer the highest approval odds for “subprime” borrowers.

- If you struggle with overspending: Choose Upgrade. Their “Direct Pay” feature ensures the money goes to your debt, not your bank account.

- If you have a “Thin” credit file (New to credit): Apply with Upstart. Their AI looks at your job and education, not just your FICO history.

- If you have a Co-Signer (Partner/Parent): Go with Prosper. Adding a co-applicant with better credit is the fastest way to lower your interest rate.

- If your score is 660+ and you want $0 fees: LightStream is the undisputed winner. Do not pay origination fees if your credit is already in the “Good” range.

Best Debt Consolidation Loans: Frequently Asked Questions

Can I get a debt consolidation loan with a 580 credit score?

Yes. Lenders like Upgrade and Upstart specifically target the 580-620 range. However, expect to pay an origination fee and a higher APR than someone with a 700 score.

Does consolidating debt hurt my credit score?

Initially, you may see a small dip due to the “Hard Inquiry.” However, once you pay off your credit cards, your Credit Utilization drops significantly, which usually results in a massive score boost within 30–60 days.

What is an origination fee?

This is a one-time fee taken out of your loan before you receive the money. For example, if you borrow $10,000 with a 5% fee, you will receive $9,500, but you will still owe back $10,000 plus interest.

Is LightStream better than Upstart?

Only if you have good credit. LightStream is cheaper (no fees), but they are much pickier. Upstart is better for those who need a “yes” when the big banks say “no.”

Is bankruptcy better than these best debt consolidation loans?

No, these loans keep credit accounts open and active (positive payment history), while bankruptcy stays 7–10 years and tanks scores 200+ points. Consolidation preserves future lending options.

Are debt consolidation loans tax deductible?

No, personal loans aren’t tax deductible (unlike mortgages). However, the $150+/mo savings from 24%→12% rates far outweighs any tax break for most Americans.

Not sure what your current score is? Read our guide on How to use Credit Karma to check your standing before you apply.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.