3 Best Premium Travel Credit Cards 2026: Chase vs Amex vs Capital One

Choosing the best premium travel credit cards is about more than just a shiny metal finish – it’s about the math of luxury.

Advertiser Disclosure: At US Finance Fix, we believe in transparency. This guide is independent and fact-checked. We may receive commissions from some of the products mentioned, but our “Alex Hale” editorial standards ensure that the math – not the commission – drives our reviews.

There comes a point in your financial journey where “cash back” isn’t enough. You want the lounge access, the travel protections, and the massive sign-up bonuses. And you start looking for your first premium credit card. But with annual fees ranging from $250 to $895, choosing the wrong card is an expensive mistake.

Not ready for a $895 fee? If your credit score is still growing or you don’t travel monthly, start with our Best Travel Credit Cards for Beginners. You can earn the same points with $0 annual fees while you build your score.

I’m Alex Hale. I don’t look at cards based on how shiny they are; I look at the net-effective cost. Today, we’re putting the “Big Three” head-to-head to find your perfect match.

| Feature | Chase Sapphire Reserve | Amex Platinum | Capital One Venture X |

|---|---|---|---|

| Annual Fee | $795 | $895 | $395 |

| Best For | Ease of Use (1.5x points) | Luxury & Lounges | Simplicity & Value |

| Core Credit | $300 Travel + $500 Hotel (The Edit) + $250 Select Hotel | $600 Hotel ($300 semiannual) + $200 Air | $300 Travel Portal + $100 worth miles |

| Top 2026 Perk | 1.5x Point Value in Portal | Centurion Lounge & 5x Flights | 10k Anniversary Miles |

| “Net Cost” (After Credits) | $495 (+ hotel credits*) | ~$0 (If you use all credits) | -$5 (They pay you to keep it) |

Alex’s Professional Note: “While the Sapphire Reserve offers over $1,500 in potential credits, I calculate the ‘Net Cost’ at $495. Why? Because the $300 Travel Credit is automatic and guaranteed for everyone. The hotel and dining credits require specific types of travel (like 2-night luxury stays). If you use those, the card is effectively free but for a beginner, $495 is the realistic ‘starting’ cost.”

The Net Cost Framework: Why Premium is Often “Free”

Don’t let a $795 sticker price scare you. In 2026, the world’s best travel cards are designed to be “self-funding” for the right traveler. Before you apply, run this simple math:

Annual Fee – (Credits You ACTUALLY Use) = Net Cost

How to interpret your results:

- Under $100: You are effectively getting luxury lounge access, $100,000 in travel insurance, and elite hotel status for the price of a Netflix subscription. This is a “Green Light” to apply.

- $100 to $300: You are “pre-paying” for travel. This only makes sense if the points you earn (the “Welcome Bonus”) are worth more than this gap.

- Over $300: Unless you are a weekly business traveler, the card is likely a net loss for you. Check out our Beginner Guide for $0 fee alternatives.

1. The Chase Ecosystem: The “Power User” All-Rounder

The Chase Sapphire Reserve® remains the gold standard for flexibility, but it now carries a $795 annual fee. While steep, it’s justified by a massive $1,050+ travel credit stack for 2026.

- The Math: You get a $300 flexible travel credit, a $500 credit for “The Edit” luxury hotels (two $250 chunks), and a one-time $250 credit for select hotel brands.

- Why it wins: Their Ultimate Rewards® points are the most valuable in 2026 because you can transfer them 1:1 to partners like Hyatt or redeem them for 1.5 cents each in the Chase Travel portal.

- Apply here

2. The Amex Lifestyle: The “Status” Membership

The American Express Platinum Card® has fully transitioned into a “luxury club membership” with a $895 annual fee. It is no longer an everyday spending card; it is a tool for those who live in airport lounges and dine at high-end restaurants.

- The Math: Between the $600 luxury hotel credit (split semi-annually), $400 Resy dining credit, and $200 airline fee credit, the card can “pay you” to keep it—but only if your lifestyle already involves these brands.

- Why it wins: Unmatched lounge access (Centurion, Delta Sky Club, Priority Pass) and instant Gold Status with Marriott and Hilton.

- Apply here

3. The Capital One Disruptor: The “Simple Math” King

The Venture X is the undisputed winner for the average traveler who hates tracking “coupon book” credits. For a $395 annual fee, it remains the most affordable way to get premium perks.

- The Math: You get a $300 travel credit (via Capital One Travel) and 10,000 anniversary miles ($100 value). Combined, these credits worth $400 effectively mean Capital One pays you $5 a year to hold the card.

- Why it wins: It’s the easiest card to manage. You earn a flat 2x miles on every purchase, making it the perfect “one-and-done” card for your wallet.

- Apply here

Best Premium Travel Credit Cards: 2026 FAQ

What credit score do I need for a premium travel card in 2026?

While a 720 FICO was the historical benchmark, most 2026 “Visa Infinite” issuers (Chase and Capital One) now look for a 740 FICO score or higher due to tighter lending standards. If your score is currently between 680 and 739, I highly recommend using my Credit Dispute Guide to clean up any “thin file” errors before risking a hard inquiry on an $895 card.

Can I have more than one premium travel card?

Absolutely—but only if you “Math the Gap.” Having both the Amex Platinum and Sapphire Reserve is a common “Pro” move, but it results in $1,690 in annual fees.

Alex’s Strategy: Only hold multiple premium cards if the Welcome Bonuses or unique credits (like the $300 Chase Travel credit vs. Amex’s $600 Hotel credit) outweigh the redundant perks like Priority Pass lounge access.

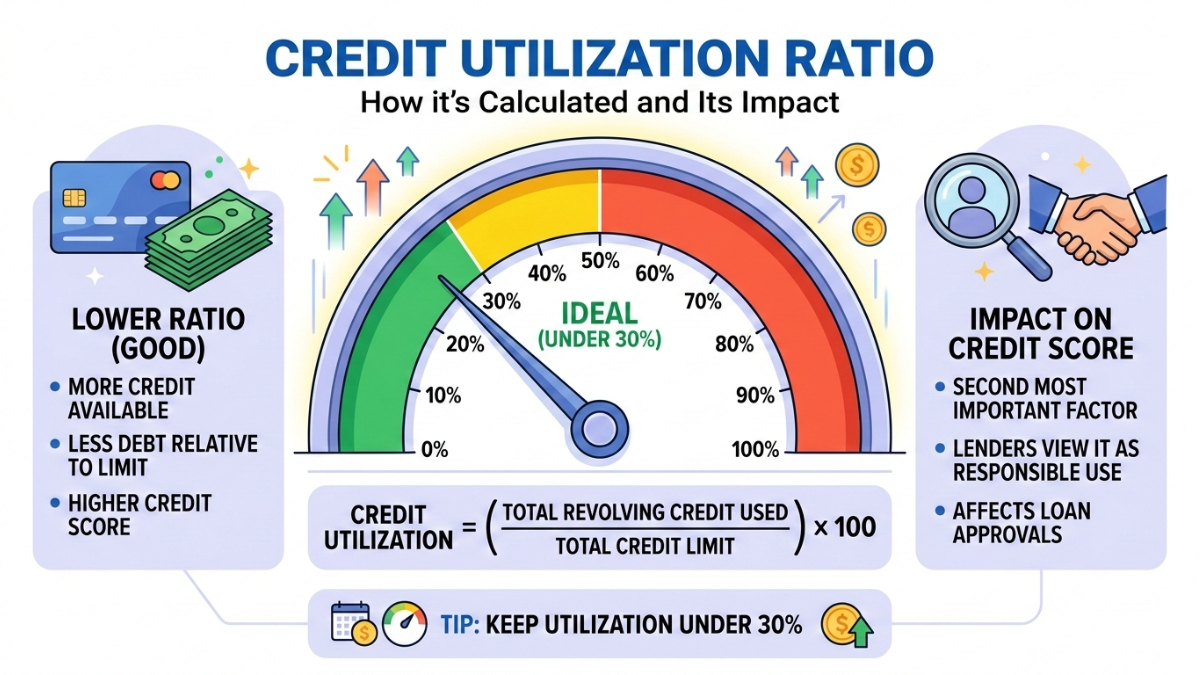

Do these cards hurt my credit utilization?

It depends on the card type. Chase and Capital One are traditional credit cards; they have fixed limits that help your utilization by increasing your total available credit. However, the Amex Platinum is a “No Preset Spending Limit” card. In 2026, most credit models still do not include Amex balances in your utilization percentage, meaning a large travel purchase on your Amex won’t “tank” your score like it would on a regular card.

Is the 2026 fee hike worth it?

With Chase at $795 and Amex at $895, these cards are only “worth it” if you are a High-Velocity Traveler. If you aren’t staying in hotels at least 4 times a year or visiting lounges monthly, you will likely lose money. For those people, I recommend our Beginner Travel Card Guide to earn the same points for $0.

Not a frequent flyer?

If you travel less than three times a year, the “Net Cost” of a premium card might not make sense. Instead of chasing travel points, you can earn up to 6% back on your daily essentials. Check out our expert guide on the Best 7 Proven US Cash-Back Credit Cards to maximize your 2026 rewards on groceries, gas, and dining.

Alex Hale is an independent personal finance researcher with a background in the US banking industry. Alex specializes in breaking down the fine print — Schumer Boxes, fee schedules, and cardholder agreements — so readers get the full picture before applying for any financial product.

More about Alex & our editorial process →Get the US Finance Fix Weekly

Join 1,200+ Americans receiving Alex Hale’s weekly breakdown of credit card secrets, debt-payoff strategies and investment opportunities.